While many types of student loan forgiveness are tax-free federally, several states may levy taxes on student loan forgiveness.

Even though some popular programs like Public Service Loan Forgiveness (PSLF) are tax free federally, every state has a different law regarding state taxes on loan forgiveness. When you add in all the other types of loan forgiveness: death, disability, borrower defense to repayment, income-driven repayment plan, and student loan repayment assistance programs… it get’s complicated.

The American Rescue Plan Act of 2021 added an exclusion from income on federal income tax returns for student loan forgiveness through December 31, 2025 – meaning all types of student loan forgiveness is tax free on the federal level.

Which States Tax Student Loan Forgiveness?

While many types of student loan forgiveness are tax-free federally, several states may levy taxes on student loan forgiveness.

Even though some popular programs like Public Service Loan Forgiveness (PSLF) are tax free federally, every state has a different law regarding state taxes on loan forgiveness. When you add in all the other types of loan forgiveness: death, disability, borrower defense to repayment, income-driven repayment plan, and student loan repayment assistance programs… it get’s complicated.

The American Rescue Plan Act of 2021 added an exclusion from income on federal income tax returns for student loan forgiveness through December 31, 2025 – meaning all types of student loan forgiveness is tax free on the federal level.

But what about state policies for taxing student loan forgiveness? Some states provide tax-free status for student loan forgiveness and some do not. This could be an unexpected tax bomb waiting for some Americans.

General Issues Of State Taxes And Student Loan Forgiveness

While student loan forgiveness is tax-free federally through December 31, 2025, it may not be tax-free on the state-level. In fact, prior to the American Rescue Plan Act of 2021, some student loan forgiveness programs were taxable on the federal level. See this guide to Federal taxes and student loan forgiveness.

Based on our research of state tax laws, you may still have to pay a “tax bomb” on student loan forgiveness to your state. In some states, the discharge of debt is considered taxable income. For example, if you have $10,000 in student loans forgiven, that amount gets added to your income, and you pay tax on the result.

Currently, we see the following:

- 9 states with no state income tax, so loan forgiveness is tax-free

- 20 states that automatically conform with federal tax rules, so loan forgiveness is tax-free

That leaves 21 states, where student loan forgiveness may or may not be tax free. Specifically, there may some types and/or timing of loan forgiveness that may be tax free, while other forms and/or timing are not.

As such, state taxes and loan forgiveness add a messy complication to student loan borrowers.

Find your state below and see what laws your state follows.

States With No Income Tax

Nine states provide tax-free status for student loan forgiveness because they do not have a personal income tax. These states include:

- Alaska

- Florida

- Nevada

- New Hampshire

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

Washington now taxes capital gains for higher earners.

States That Automatically Conform With Federal Tax Rules

There are 20 states that base their definition of income on the federal definition of adjusted gross income (AGI) from the Internal Revenue Code of 1986, as amended, and automatically update their definition with changes in federal law.

What Does This Mean: Changes in federal tax law, such as the new exclusion from income for student loan forgiveness, will automatically affect state income tax in these states. Therefore, whatever happens at the federal level for student loan forgiveness will automatically happen at the state level.

While many types of student loan forgiveness are tax-free federally, several states may levy taxes on student loan forgiveness.

Even though some popular programs like Public Service Loan Forgiveness (PSLF) are tax free federally, every state has a different law regarding state taxes on loan forgiveness. When you add in all the other types of loan forgiveness: death, disability, borrower defense to repayment, income-driven repayment plan, and student loan repayment assistance programs… it get’s complicated.

The American Rescue Plan Act of 2021 added an exclusion from income on federal income tax returns for student loan forgiveness through December 31, 2025 – meaning all types of student loan forgiveness is tax free on the federal level.

But what about state policies for taxing student loan forgiveness? Some states provide tax-free status for student loan forgiveness and some do not. This could be an unexpected tax bomb waiting for some Americans.

General Issues Of State Taxes And Student Loan Forgiveness

While student loan forgiveness is tax-free federally through December 31, 2025, it may not be tax-free on the state-level. In fact, prior to the American Rescue Plan Act of 2021, some student loan forgiveness programs were taxable on the federal level. See this guide to Federal taxes and student loan forgiveness.

Based on our research of state tax laws, you may still have to pay a “tax bomb” on student loan forgiveness to your state. In some states, the discharge of debt is considered taxable income. For example, if you have $10,000 in student loans forgiven, that amount gets added to your income, and you pay tax on the result.

Currently, we see the following:

- 9 states with no state income tax, so loan forgiveness is tax-free

- 20 states that automatically conform with federal tax rules, so loan forgiveness is tax-free

That leaves 21 states, where student loan forgiveness may or may not be tax free. Specifically, there may some types and/or timing of loan forgiveness that may be tax free, while other forms and/or timing are not.

As such, state taxes and loan forgiveness add a messy complication to student loan borrowers.

Find your state below and see what laws your state follows.

States With No Income Tax

Nine states provide tax-free status for student loan forgiveness because they do not have a personal income tax. These states include:

- Alaska

- Florida

- Nevada

- New Hampshire

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

Washington now taxes capital gains for higher earners.

States That Automatically Conform With Federal Tax Rules

There are 20 states that base their definition of income on the federal definition of adjusted gross income (AGI) from the Internal Revenue Code of 1986, as amended, and automatically update their definition with changes in federal law.

What Does This Mean: Changes in federal tax law, such as the new exclusion from income for student loan forgiveness, will automatically affect state income tax in these states. Therefore, whatever happens at the federal level for student loan forgiveness will automatically happen at the state level.

These states include:

- Connecticut

- Delaware

- Illinois

- Iowa

- Kansas

- Louisiana

- Maryland

- Massachusetts

- Michigan

- Missouri

- Montana

- Nebraska

- New Mexico

- New York

- Ohio

- Oklahoma

- Rhode Island

- Utah

- Vermont

- Washington, D.C.

Massachusetts and Michigan use a hybrid approach, with taxpayers being able to choose to use the federal AGI. In addition, Iowa has a subtraction from state income for military student loan repayment.

New York has an explicit subtraction for student loan death and disability discharges.

Three states base their definition of income on the federal definition of taxable income instead of AGI and automatically update their definition with changes in federal law. These states are Colorado, North Dakota and Oregon.

States That Conform With Federal Tax Rules As Of A Specific Date

There are several states that must pass laws to incorporate changes in the Internal Revenue Code of 1986 (IRC). Not all will. Even when they do, the state laws may lag changes in federal law by a year or more.

What Does This Mean: It means that, depending on the type of loan forgiveness AND the date of the loan forgiveness, it may or may not be taxable. While many of these states are currently tax-free for student loan forgiveness, that may change. It may also only apply to certain reasons for loan forgiveness.

One must compare the date of the version of the IRC upon which the state tax law is based with the date upon which the tax-free status was enacted for various student loan forgiveness and discharges.

In effect, these states have decoupled their definition of income from the federal definition of income. Accordingly, these states do not automatically include the exclusion from income for student loan forgiveness from the American Rescue Plan Act of 2021 (ARPA).

Student loan forgiveness may be taxable in these states, depending on the date you receive student loan forgiveness and when the state changes the law.

States That Conform With The Federal Definition Of “AGI” As Of A Specific Date

There are 12 states that base their definition of income on the federal definition of adjusted gross income (AGI) as of a specific date. These states are:

- Arizona

- California

- Georgia

- Hawaii

- Indiana

- Kentucky

- Maine

- North Carolina

- Pennsylvania

- Virginia

- West Virginia

- Wisconsin

Arizona does not have an addition to income for student loan forgiveness and other student loan discharges.

California provides tax-free status for death and disability discharges through January 1, 2026. Public service loan forgiveness is tax-free in California, as is forgiveness connected to an income-driven repayment plan. Note: Tax-free status for borrower defense to repayment and closed schools discharges expired in 2024, and it’s unclear if it will be extended.

Hawaii conforms to the American Rescue Plan Act as of 2024.

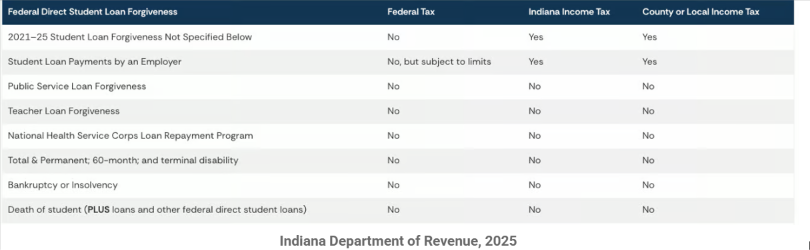

Indiana is mixed depending on the reason for the loan forgiveness. The Indiana Department of Revenue has a chart:

Kentucky conforms to the federal ARPA as of December 31, 2023 for student loan forgiveness.

Maine provides a state income tax credit, the Opportunity Maine Tax Credit, to reimburse student loan payments for recent college graduates who live and work in Maine. Maine also provides a subtraction for student loan payments made by the borrower’s employer under the Maine Educational Opportunity Program (FAQ).

North Carolina: Employer student loan repayment assistance programs (LRAPs) are taxable in North Carolina since 2020.

Pennsylvania provides tax-free status for student loan debt that is forgiven via a state or Federal program that provides for payment or cancellation of student loans when the work is done for a period of time in a specified profession as of 2021. This would include Public Service Loan Forgiveness (PSLF) and LRAPs like the Student Loan Relief for Nurses (SLRN) program. See the updated tax bulletin here.

Virginia recently updated their definition of taxable income to conform to the IRS IRC as of December 31, 2021. This means that as of January 1, 2022, student loan forgiveness is excluded from taxable income through December 31, 2025. See this updated tax bulletin.

Wisconsin specifically excludes from income total and permanent disability (TPD). It also appears to exclude PSLF, since PSLF exclusion appears in 26 USC 108(f)(1) – which is the same section as TPD. However, Wisconsin has elected to INCLUDE any debt forgiven under the “special timeframe of December 20, 2020 through January 1, 2026″ under IRC sec. 108(f)(5). This means that debt forgiven under this section, like income-driven repayment plans” is included income.

States That Conform With The Federal Definition Of “Taxable Income” As Of A Specific Date

Three states base their definition of income on the federal definition of taxable income instead of AGI as of a specific date. These states are Idaho, Minnesota and South Carolina.

Minnesota generally conforms with federal law concerning the taxation of student loan forgiveness. Minnesota has a subtraction for the forgiveness after 20 or 25 years in an income-driven repayment plan and for Minnesota Teacher Shortage Loan Forgiveness. Minnesota provides a nonrefundable student loan credit for payments made on qualified student loans.

This table shows the effective date of changes to the Internal Revenue Code of 1986 or Higher Education Act of 1965 to exclude certain types of student loan forgiveness from income. Comparing the date of the version of the IRC to which the state conforms with these dates may provide an indication as to whether each type of loan forgiveness is tax-free.

States That Do Not Base Income On Federal Tax Rules

Four states base their definition of income on their own definition of gross income. These states do not conform with the federal definition of income. Any changes in the federal definition of income will not affect these states.

What This Means: You have to know the state rules. That doesn’t mean that loan forgiveness is taxable (though it is in several of these states).

The exclusion from income for student loan forgiveness from the American Rescue Plan Act of 2021 does not apply to these states. These states must pass laws to exclude student loan forgiveness from income.

Accordingly, student loan forgiveness may be taxable in these states.

These states are:

- Alabama

- Arkansas

- Mississippi

- New Jersey

Alabama currently follows federal law for the treatment of debt cancellation – including student loan forgiveness.

Arkansas has a subtraction for interest paid on qualified education loans. PSLF is excluded from income (i.e. not taxable). Other types of loan forgiveness (like IDR-driven forgiveness) are taxable.

New Jersey has an exclusion from income for the cancellation of debt. That means that cancelled debt, such as student loans, are not taxable.

For Public Service Loan Forgiveness (PSLF) specifically, Mississippi is currently the only state that taxes PSLF loan forgiveness.